Pensions & Retirement accounts

Maine tax laws conform with Federal laws except in a few areas. Retirement account contributions and distributions ALMOST always present the situation where manual entries in the Maine section of the tax software are necessary because of differences in the treatment of these items at the state and federal levels.

Below is a general explanation of

Maine Pension Income Deduction on Schedule 1 - Income Modifications and

The most confusing area of nonconformity; the treatment of the contributions into & distributions from the Maine Public Employees Retirement System, commonly referred by its acronym MPERS (em - pers).

General Pension information and explanations can be found on the

FEDERAL - Retirement Income page of this site.

What do I need to know?

Maine tax law allows for a pension income deduction to all its pensioners on Schedule 1.

Maine does not tax active Military pensions - AT ALL. Full stop!

Maine Public Employees Retirement System (MPERS) distributions need your special attention.

Maine Tax Return Begins with Federal AGI

(Review the discussion about Differences with Federal taxes.)

The deferred income that is in retirement accounts, like an IRA or a 401(k), will be taxed in the year the taxpayer accepts distributions from these accounts. The tax treatment at the federal level of these retirement distributions is addressed in Pub 4491, Chapter 18 - Pension Income and on this site at Federal - Retirement Income.

Retirement distributions need to be reviewed to ensure a proper reconciliation with Maine law occurs. We account for any differences that exist with Federal level treatment on Schedule 1 - Income Modifications.

Maine lawmakers got together and agreed on a few things related to pension & IRA distributions that are different than those decided by Federal lawmakers. It’s as if Maine lawmakers said:

““We think it’s a good idea to provide relief to our pensioners in light of the fact that their incomes are essentially fixed. We will omit from taxation, the first $10,000 of pension income. However, if the taxpayer receives $10,000 in untaxed Social Security benefits, then we will consider the relief achieved.””

3 Pension related DIFFERENCES with Federal law.

Because of these differences the tax preparer will need to look at each item of retirement income to determine whether a manual entry is required in the tax software.

Making entries on the manual entry checklist while completing the Federal return will inform your manual entries in the Maine section.

There are 3 Pension related Differences with the federal tax law that can be ‘remedied’ with manual entries.

Determine the Pension Income Deduction. Maine allows each of its pensioners to deduct $10,000 in pension income. (Subtraction from Income) You will make a manual entry in tax software for this amount.

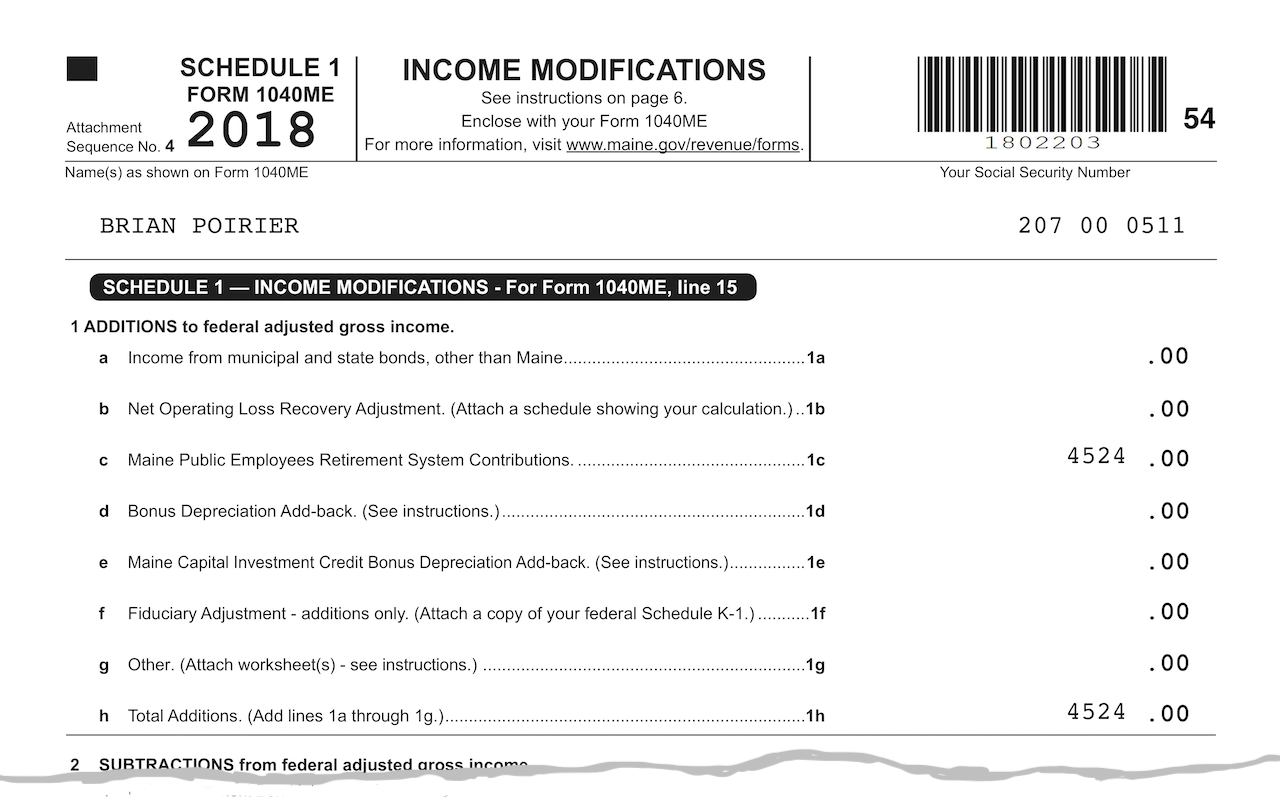

Determine whether pension contributions were made to MPERS. This is a little tricky. Maine taxes these contributions in the year they are made. This is a manual entry in the tax software as an Addition to Income on Schedule 1, Line 1c.

Determine whether pension distributions were made from the MPERS. This, too, is a little tricky. (see image below for sample MPERS 1099-R)

Because, unlike at the Federal level, Maine has already taxed a portion of these pension distributions in the year they were contributed, a portion of this pension distribution is NOT subject to Maine tax.

This portion, or allocated amount determined by actuarial formula, of the pension distribution is a manual entry in the tax software as a Subtraction from Income on Schedule 1, Line 2f.

Pension Income Deduction

As already mentioned, Maine allows each of its pensioners to deduct $10,000 in pension income. (Schedule 1 - Subtraction from Income, Line 2d)

This is a manual entry in the tax software using the amount shown in Box 14. (See image below at right). In the case that Box 14 is blank, you will use the amount in Box 2a.

Notice that Maine will first consider whether the pensioner has received $10,000 in Social Security Benefits. The reduction is considered to have happened at the Federal level. See image below 2018 - Worksheet for Pension Income Deduction in Spouse column

On the Maine return, to the degree that SS benefits were taxed on the Federal return, you will see those taxable SS benefits being shown as a subtraction on Maine Schedule 1 (this step is handled automatically by the tax software).

This action will factor into the Pension Income Deduction formula so it may not appear that the $10,000 Pension Income Deduction from Income is being properly calculated. Refer to the worksheet that is generated as part of the Maine return.

Use the amount in Box 14 for Pension Income Deduction

Active Military Pensions are not taxable in Maine

Entry screen using 1099-Rs at left

Entries made on the Checklist

Manual entries made in the Pension Income Deduction screen displayed here on the Worksheet

What is MPERS?

MPERS is the Maine Public Employees Retirement System. Just like it sounds, this is a retirement system for Maine employees. In most cases, employees do not choose to contribute to this Pension system. It is the state’s alternative to the Social Security system. (MPERS handbook)

The following statements are from a resource document found at mainepers.org.

Retirement contributions made as an employee make up a portion of the benefits received each month in retirement.

Contributions on which taxes were already paid are not taxed again in retirement.

Retiree already paid Maine state taxes on all of their contributions. Retiree paid Federal taxes on contributions made before January 1, 1989.

Retiree has not paid Federal or State taxes on the interest their contributions earned while they were working.

Contributions to the MPERS pension.

Contributions to the MPERS pension.

To follow federal tax law relating to pension contributions, the MPERS contributions have been removed from taxable income at the Federal level.

Therefore, Federal - AGI (the beginning number on the Maine return) has the “tax-favored” pension contributions removed.

However, Maine law asserts that no special tax treatment will be allowed at the time the contributions are made but an allowance will be made at the time of distribution such that none of the earnings will be taxed twice.

Usually, you can see evidence of this on the W-2 of a state employee paying into MPERS.

Below is the image of the W-2 for an employee of the Brunswick School Dept., notice:

pension contribution in box 14 of $4,524 to MPERS

state wages in box 16 are for the full amount of wages $58,524

federal wages in box 1 represents the total state wages LESS the tax favored retirement contributions to MPERS.

the social security wages in box 3 is blank because state employees paying into MPERS do not pay into social security.

Therefore, MPERS contributions must be ADDED back in on the Maine return.

This addition is now handled automatically by the tax software.

A proper modification to income will be ADDED to Schedule 1:

Distributions from the MPERS pension.

MPERS - FAQs for 1099-Rs - 2018 MPERS - After you retire brochure

Because of the prior Maine state taxation of contributions into the MPERS pension, a taxpayer’s 1099-R may show a difference in the Federal taxable amount shown in Box 2 and the Maine taxable amount shown in Box 14.** This will require a manual entry in the Maine module of TaxSlayer.

It may be best to highlight what is ‘at play’ here with an example of a typical retired couple.

Scenario: A retired couple, residents of Maine, are each receiving their Maine Retirement System pensions and a small amount in Social Security benefits. To make this example really interesting, they own their home and have a very high property tax bill - we’ll check to see if they are eligible to receive the Property Tax Fairness Credit. See section below for input screens and sample tax return.

** - Do not be alarmed if there is also a difference between amount in Box 1 and Box 2a. This does not concern you, with regard to preparing the Maine return. The difference between Box 1 and Box 2a represents employee contributions already taxed at the federal level and is equal to the amount shown in Box 5.

Typical 1099-R from MPERS

Please refer to the image below of the MPERS issued 1099-R.

In the Federal Section of the TaxSlayer software you simply transcribe what you see in each box.

In the Maine section, you are making manual entries to achieve two things (both from the Subtractions from Income screen):

The Pension Income Deduction. A manual entry will be made using the Maine State wages found in Box 14 of 1099-R. (see below)

‘Pick-up' Contributions’. Subtract the amount in Box 14 from Box 2a.

(14,180.32 - 12,890.97 = $1,289.35)

Sample 1099-R from MPERS

Provided here is an explanation of the amounts in Boxes 1, 2a, 5 & 14.

#1 - The actual distribution made to the retiree throughout the year.

#2 - The taxable amount shown on the Federal tax return. Notice the difference between Box 1 & Box 2a is the amount in Box 5.

#3 - The amount of contributions to the pension that have already been taxed at the Federal level. It is possible for Box 5 to be empty.

#4 - The amount that is subject to tax by the state of Maine. If you would like to know how MPERS determines this amount here is a link to that explanation & calculation.

Typical 1099-R issued by MPERS. Yes. It’s a lot to process :-)

Screenshots to illustrate software inputs in the Maine section for the sample scenario.

Click here for the sample tax return rendered from the following entries for a typical retired couple :

FEDERAL section of tax software

Two 1099-R statements received

Two Social Security Benefit Statements received (Taxpayer - $5,732, Spouse - $1,311)

MAINE section of tax software

Pension income deduction (in the Subtractions from Income section)

Pick-up Contributions (in the Subtractions from Income section). This amount is the difference between Box 2a and Box 14.

NOTE: With more than one MPERS 1099-R, add the amount from all 1099-Rs together. In this example, the 2 amounts added together for the manual entry is $2,115. See screenshot below.Finally, enter the property taxes that were paid during the year; they are extremely high. From the Credits menu, select Property Tax Fairness Credit and enter $10,388.

2 MPERS issued 1099-Rs for our typical retired couple (below)

After making our manual entries, the tax return should look like this -

SAMPLE tax return (click)

Starting at the ‘Subtractions from Income’ menu in the Maine state section of TaxSlayer SELECT

*1. Pension Income Deduction. (image below)

Maine > Subtractions From Income > Pension Income Deduction

*2. Pre-taxed State Retirement System Pickup Contributions. (image below)

Refer to each MPERS 1099-R.

Pick-up Contributions = (Box 2a) - (Box 14)

Maine > Subtractions From Income > Pretaxed State Retirement System Pickup Contributions

Finally, from the Credits menu Select

Property Tax Fairness Credit

See image below for manual entries.

Maine > Credits > Property Tax Fairness Credit

The necessary modifications have now been made to prepare an accurate Maine return.

Close out of the Maine return by following the screen prompts at the bottom of each page.